Magic Formula (Part V)

The Magic Formula is a two Factor Model that looks at companies with the best earnings yield and return on capital. While this strategy is fundamentally strong in concept, there were several areas of concern:

- Differences in screen attributes can make a big impact on the universe of securities in the portfolio.

- Recent underperformance in value investing may suggest crowding in the strategy, and caution may be prudent.

- Our backtests differ substantially from investments made by Greenblatt as part of his Gotham Long/Short Equity funds.

We conclude that the Magic Formula is an excellent strategy to learn about value investing, the merits of factor investing, and ideas of what to look for when

Get the Book: The Little Book that Beats the Market

Parts:

One , Two , Three , Four , Five

Some Final Thoughts on The Magic Formula

The concept behind finding good companies that are cheap is one that makes intuitive sense and appeals to those of us who look to unlock misplaced value in a world dominated by passive investments. On top of that, having a very specific and relatively easy approach to define these two factors makes the Magic Formula a uniquely attractive opportunity for both novice and sophisticated investors alike. There are, however, some areas of caution.

-

Your Mileage May Vary

While we proposed one way in measuring out the factor rankings, we find that small variations in looking at return on capital or minute changes in our screen can result in substantially different stock holdings. As noted, we were unable to fully replicate the symbol list provided by the official strategy screener. In addition, some of the "extra" screening criteria suggested by Greenblatt (i.e, eliminate stocks with P/E below 5), conflicts with the portfolio output observed from magicformulainvesting.com. As such, our analysis is at best an approximation, and research published by others online will also likely suffer from these discrepancies.

-

Drawdowns Matter

One of the suggestions on why everyone doesn't use this method of investing if it seems so easy and obvious is that investors are unwilling or unable to hold through temporary losses and underperformance. But it's no secret that strategies that once worked may experience alpha deterioration over time, as investors crowd into the trade and returns are reduced. There's some notion that a strong company that is also cheap will always be a strong, cheap, company, but what if a security is cheap due to underlying factors not measured within the parameters of the Magic Formula? The term "value trap" comes up often when looking at companies that seem like an exceptional opportunity relative to its peers, but is in fact marred by weakness not immediately observed without a deeper understanding of its cash flows and business operations. In these scenarios, a bigger portfolio may help diversify away weaknesses in these value traps while maintaining the edge provided by the conceptually strong two factor model. We may also look into each company in detail, but then the simplicity of the model itself becomes eroded.

-

Magic vs Gotham

When Greenblatt is not spending his time writing on how to make us all incredibly wealthy or teaching young guns how to be the next Buffett at Columbia, he manages a multi-billion dollar hedge fund called Gotham Asset Management LLC. While we see that the funds deployed strategies that have a value bent, Gotham operate quite differently from the Magic Formula. For one, many of the equity funds are Long/Short, meaning that the managers buys attractive stocks and short overvalued companies, with the construction of Gotham funds being a net long exposure of around 50-60% (i.e. 120% Long - 60% Short).

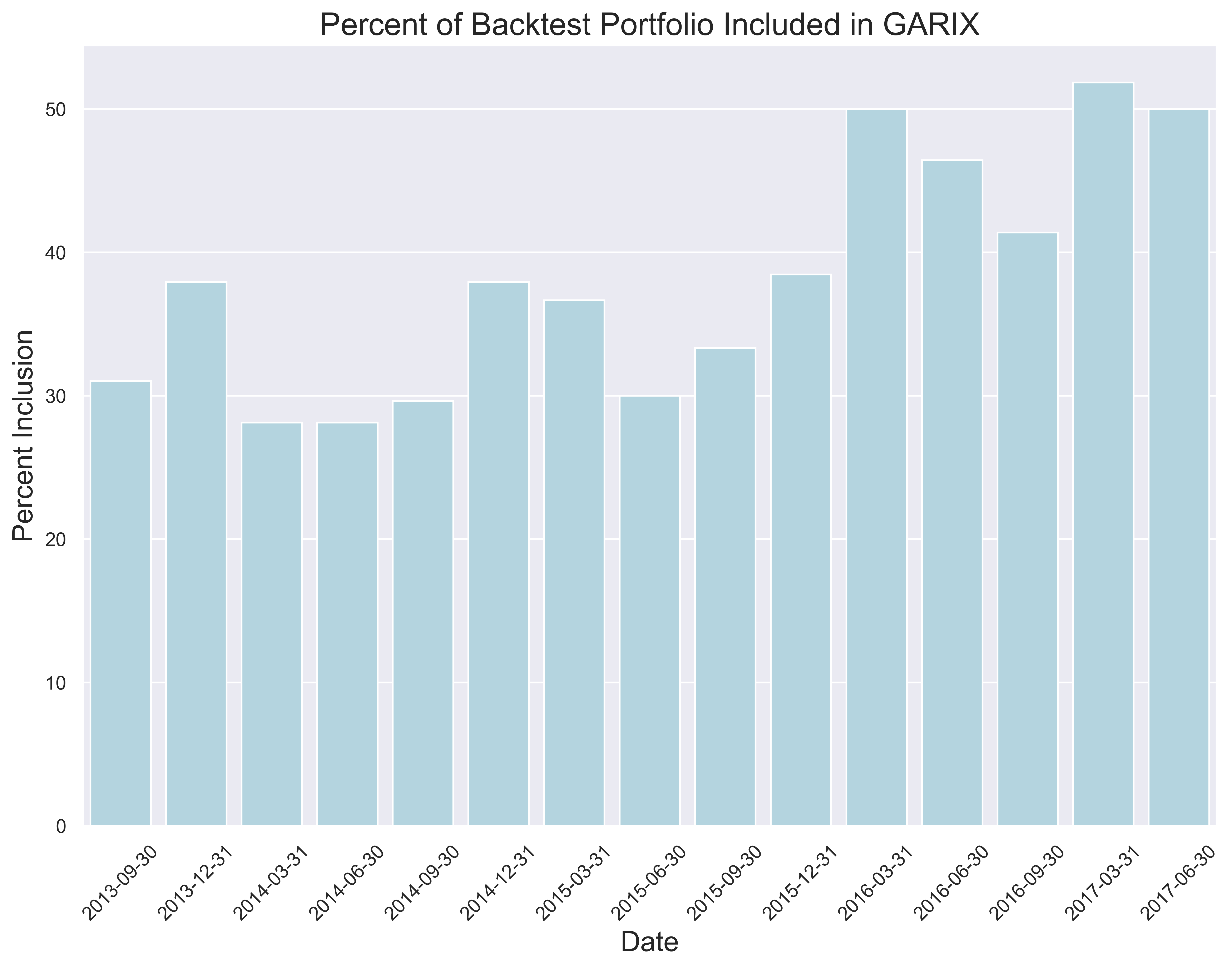

If we look at the performance of Gotham Absolute Return Institutional (GARIX) as of 06/30/2020, we see that it has a cumulative return of 50.48% since inception (August 31st, 2012) compared to a return of 159.19% on the S&P 500. The fund is also widely diversified, with a portfolio composition of 647 Long Securities with 453 Short Securities.

With the 13F data submitted to the SEC, we can dig a bit deeper to how Gotham compares to our Magic Formula Screen. We take a look at our constructed portfolio to compare the similarity between the symbols included in our backtest against the holdings reported quarterly to the SEC (note that 13Fs do not include short positions). Because GARIX is substantially more diverse, we ask the simple question of "How many securities in our constructed portfolio was also found in GARIX?" We look at quarterly data reported between the third quarter of 2013 until the second quarter of 2017. Our results show that roughly a third to a half of the securities in our portfolio was also found in GARIX.

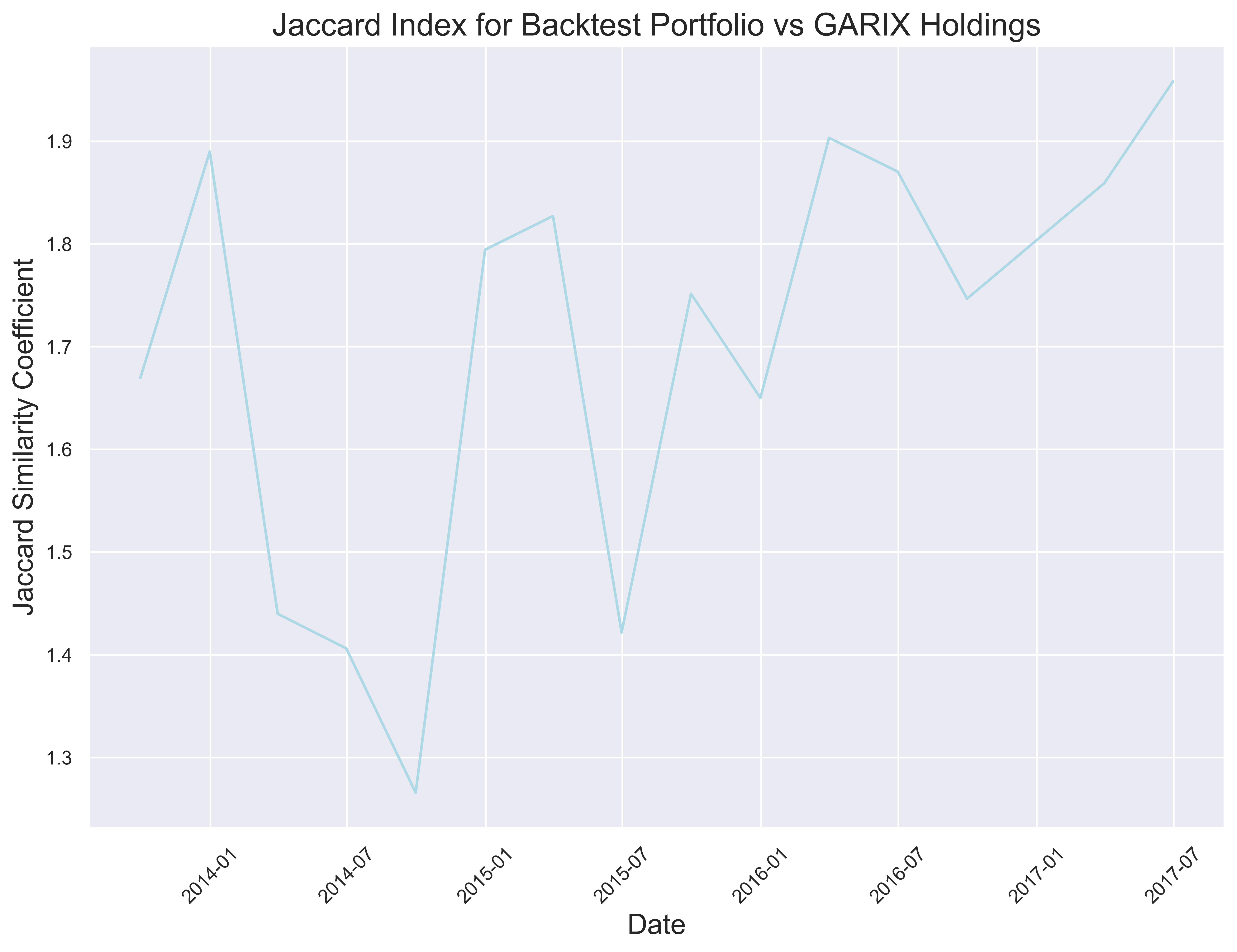

A secondary way to measure portfolio similarity is using the Jaccard Similarity Coefficient, which is a statistical measure of sample set similarity based on the size of the interaction between the samples divided by the size of the union in the two data. Because of the vast difference in portfolio sizes, the Jaccard values come up expectedly low. We can do some work on weighting our portfolio values differently, but with such a large difference in the size of these portfolios, the value of such a comparison is likely limited.

Concluding Remarks

So where do we go from here?

In this exercise, we looked at a simple two factor model of investing and investigated the merit behind the signals, using Python for most of our analytics, often leveraging the tools built into Quantopian. We reconstructed the Magic Formula screen, tested the predictive power of the alphas, backtested it's performance, and discussed our results relative to the author's investment management.

In the end, we found positive Sharpe indicative of a signal worthy of further study, but perhaps with results that are not as robust in recent years. Whether this comes from an overcrowding of the trade or whether it is just a temporary underperformance remains unknown, but we do feel that the simplicity of the strategy makes it a suitable signal to work with in your own research.